China’s Property Slump Can Curb Growth for Years, Even Without a Banking Crisis

China’s Property Slump Can Curb Growth for Years, Even Without a Banking Crisis [ 5 min read ]

INSIGHTS

- New analysis of nationwide prefecture-level data in China and Japan finds that investment overhang, consumption wealth effects, and poor consumer sentiment curbed growth for years after each country’s property bust — effects that occur independently of a banking crisis.

- Cities in China more reliant on real estate investment have seen annual GDP growth run about 2 percentage points lower since 2019 than comparable cities with less exposure — echoing the decade-long negative returns Japan suffered after its 1991 property crash.

- Real estate makes up nearly 70% of China’s household wealth — double the U.S. share. The analysis finds a 10% drop in home prices cuts China’s household spending by roughly 1.5–2.3%, versus just 0.6% in 1990s Japan. Applied to China’s 20% (official) to 40% (unofficial) property price declines, that’s a consumption loss of 2–4% of GDP.

- Sentiment matters too: an AI analysis of local news shows that in cities with more pessimistic housing-market news coverage, the estimated consumption hit from falling prices was roughly double that of cities with less negative coverage.

- Six years into its adjustment, China could be roughly halfway through if it follows Japan’s trajectory (an eventual 60% price decline) or two-thirds through if it follows the milder path the U.S. took after 2008.

Read this brief on SUBSTACK

At its peak in 2019, the real estate sector accounted for nearly a third of China’s total economic activity. A new analysis compares China’s housing downturn, now in its sixth year, to Japan’s 1990s real estate bust — despite important institutional differences, from land ownership (private in Japan, state-owned in China) to how real estate debt is structured (corporate borrowing in Japan, local government financing vehicles in China) to the fact that China’s state-dominated financial system has so far kept the downturn from becoming a banking crisis the way Japan’s did. The comparison holds up, the analysis argues, because the drag on growth runs mainly through three “real” channels — investment overhang, consumption wealth effects, and sentiment — that operate independently of bank balance sheets. Data from Japan’s decades-long adjustment offers clues for how long China’s property downturn can be expected to cut into growth.

The data. The researchers build a city-level dataset covering nearly 300 Chinese prefecture-level cities from 2000 to 2024, tracking real estate investment, housing stock, consumption, and housing prices. The researchers pair this dataset from China with a comparable historical dataset for Japan’s 47 prefectures, in some cases reaching back to the 1950s. For both datasets, the analysis isolates the part of each city’s real estate investment driven by national trends rather than local conditions, to estimate how sensitive each city is to swings in the property cycle — a sensitivity that shows up as a boost to growth during the boom years and a drag on growth during the bust. To gauge how optimistic or pessimistic the public feels about housing, the authors use an AI model to score the tone of national daily news coverage of the housing market on a 0–100 scale, then weight those scores by local Baidu search activity, a proxy for how closely each city was tracking the coverage, to build a city-level sentiment index.

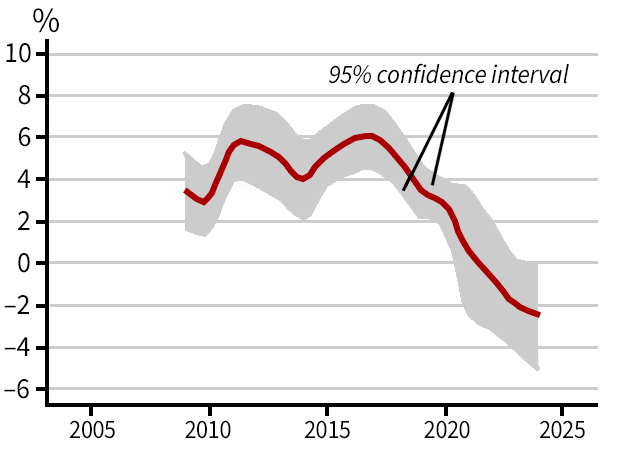

Property investment returns have gone negative. China’s real estate investment, once a reliable driver of local growth, now functions as a drag. Cities that built up the largest stockpiles of housing during boom years are growing more slowly today — consistent with an “investment overhang,” in which durable, hard-to-shed housing capital keeps dragging on prices and new building long after construction stops. Investment’s contribution to growth fell by roughly a third after the 2008 financial crisis, flattened during the mid-2010s “shantytown redevelopment” boom, and turned outright negative after 2019. Japan traced an almost identical arc, with real estate investment turning into a statistically significant drag within a year or two of its 1991 peak and remaining so through the late 1990s, only beginning to recover after 1998–99.

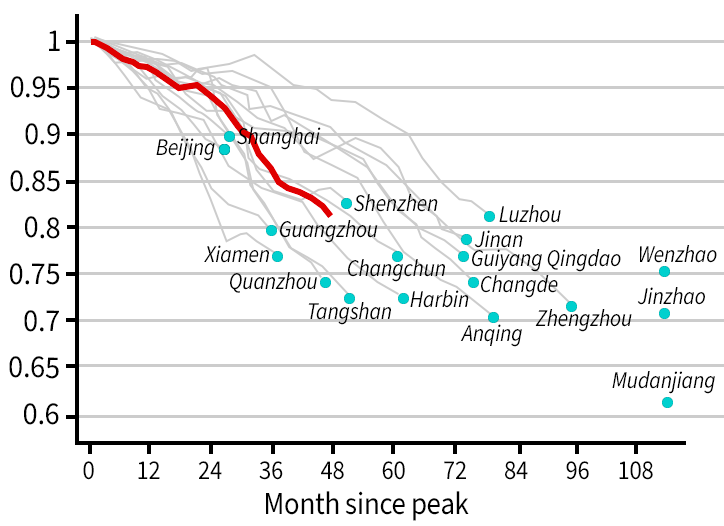

Cumulative monthly house price declines from peak (peak=1)

Sources: National Bureau of Statistics of China and authors’ calculations

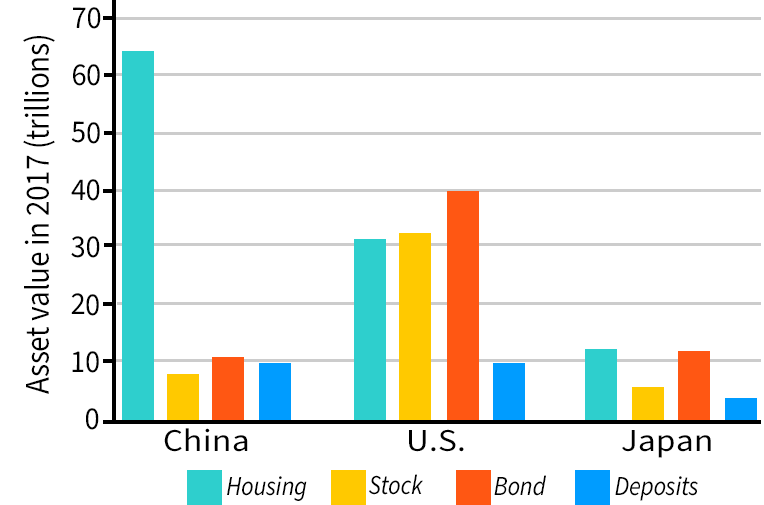

Household consumption in China is more exposed to real estate than in Japan. FFalling home values make households feel poorer, prompting them to pull back spending even when their income hasn’t changed — known as the consumption “wealth effect.” Because households in China hold close to 70% of their wealth in housing, with limited alternative places to put their money due to capital controls, and because China lacks the kind of social safety net that lets households smooth over income shocks, the wealth effect hits unusually hard there: a 10% drop in home prices cuts household spending in China by roughly 1.5–2.3%, versus just 0.6% in 1990s Japan. Applied to China’s 20% (official) to 40% (unofficial) housing price declines, that implies a consumption loss of 2–4% of GDP — dwarfing the scale of China’s current stimulus measures like consumption vouchers (under RMB 10 billion) and trade-in subsidies (about RMB 150 billion). In Japan, where wealth was split more evenly between housing and the stock market, the same price decline produced a smaller consumption response — even though the total value of Japanese land assets erased in the crash left many households with mortgages exceeding the value of their homes.

Valuation of different asset classes

Sources: World Bank, BIS, National Bureau of Statistics of China, Bank of Japan, FRED, Zillow, and authors’ calculations.

Real estate pessimism further dampens household consumption. Beyond lost housing wealth itself, the analysis finds a separate sentiment effect at work. To measure the sentiment effect, the authors use an AI model to score how pessimistic or optimistic China’s national housing news is each day, then combine that with local search data to track how closely residents in each city are actually following housing news: cities paying more attention to pessimistic coverage are treated as more exposed to bad housing news than cities paying less attention. In cities with more attention to pessimistic coverage, the estimated consumption hit was roughly double that in cities with less attention to negative coverage — a feedback loop echoing the lasting pessimism Japanese consumers felt after their own bust, and one easy to overlook next to more conventional drivers of consumption.

Real estate investment returns in China

Sources: National Bureau of Statistics of China and authors’ calculations

A downturn that doesn’t need a banking crisis to keep biting. China’s government has more control over its banks than Japan’s did, giving it tools to slow the pace of adjustment: it can let banks avoid writing off bad loans and keep lending to troubled developers and local governments rather than forcing a reckoning all at once. That keeps a banking crisis at bay. But the evidence on investment, consumption, and sentiment suggests those tools only manage the financial side of the bust — bank losses and credit flows. They do not fix the drag coming from the real economy: weaker construction activity, poorer households, and gloomier expectations, all of which keep weighing on growth regardless of how healthy the banks look. Six years in, China could be roughly halfway through if it follows Japan’s path (an eventual 60% price decline) or two-thirds through if it follows the milder U.S. post-2008 path. China also faces a faster-aging population than Japan did at a comparable stage of development, and a lower starting income level, both of which could make the adjustment harder to absorb — even as strength in AI and advanced manufacturing offers some offsetting momentum. The authors argue that without deeper reform to shift growth away from investment and toward consumption, the drag from these real channels alone could keep weighing on the economy for years, banking crisis or not.