Excess Men and Credit-Starved Firms: Underappreciated Drivers of China’s Trade Surplus

Excess Men and Credit-Starved Firms: Underappreciated Drivers of China’s Trade Surplus [ 5 min read ]

INSIGHTS

- New research posits that the “usual suspects,” like industrial subsidies, an undervalued currency, and import barriers, are not the dominant drivers of China’s roughly $1 trillion trade surplus.

- China’s skewed sex ratio is a major, underappreciated factor: families with sons save enormously to afford marriage with relatively scarce females, explaining as much as half of the rise in China’s high household savings rate, which cuts into demand for imports.

- Limited credit access for high-productivity, non-state-owned firms forces many of them to self-finance investment out of retained earnings, inflating corporate savings and, by extension, the trade surplus.

- A weak housing market has temporarily depressed imports since 2021, but this cyclical effect cannot explain surpluses recorded well before the property downturn began.

- Remedies from trade partners, like tariffs, are unlikely to blunt these structural drivers of China’s trade surplus.

Source Publication: Chang Ma and Shang-Jin Wei (2026). The Chinese Current Account Imbalances: Puzzles, Patterns, and Possible Causes. National Bureau of Economic Research working paper.

Read this brief on SUBSTACK

China’s trade surplus has been a persistent source of friction with its trading partners, peaking at nearly 10% of GDP in 2007 before settling around 2% in recent years — still a substantial sum (roughly $1.2 trillion) given the size of China’s economy. Much of the public debate blames the surplus on deliberate government policies: industrial subsidies that favor exporters; an undervalued currency; and/or barriers that keep out foreign goods. A new analysis highlights other structural factors that appear to be driving China’s trade surplus that may limit the efficacy of tariffs and other remedies imposed by China’s trading partners.

The data. The authors work relies primarily on two sources of China’s trade statistics — one from Customs, which records the physical movement of goods, and one from China’s State Administration of Foreign Exchange (SAFE), which records changes in ownership consistent with international balance-of-payments standards. The bulk of the analysis instead synthesizes a decade of academic research on China’s savings behavior — studies using household surveys, regional demographic data, and firm-level financial records — which the authors argue is the more important piece of the puzzle.

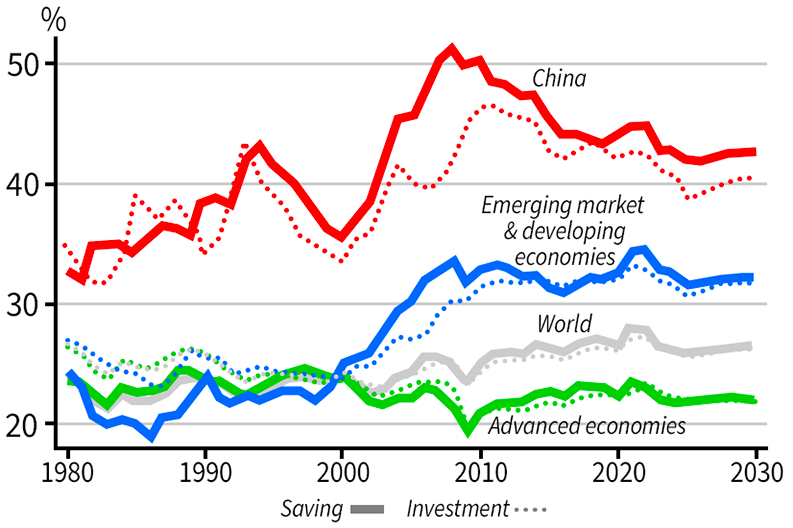

The limits of blaming industrial subsidies, currency devaluation, and the property crash. China runs thousands of industrial subsidy programs, and these have likely helped sectors, like shipbuilding and electric vehicles, capture larger global market shares. But the author’s cite economic theory to point out that across the entire economy these policies may not be enough to explain the lion’s share of China’s trade surplus: subsidies on exports tend to draw talent and capital away from firms competing with imports, causing imports to also rise in tandem with exports. China’s import-to-GDP ratio is higher than America’s, the authors point out. At the same time, high savings can produce the same effect as an undervalued currency because savers spend less on local goods, keeping local prices low relative to the rest of the world even without any currency intervention. China’s property downturn may be depressing household spending and temporarily widening the trade surplus. However, China’s surpluses were even larger in 2007, suggesting that housing weakness helps explain recent trends, not the broader multi-decade pattern. The goal of the analysis is not to dismiss these factors, but to highlight deeper structural drivers that are often overlooked.

China’s saving and investment (% of GDP)

A scarcity of brides fuels China’s savings glut. Decades of son preference in China have left a measurable surplus of young men relative to young women in the prime marriage-age population. The authors draw on prior research showing that this imbalance pushes up household savings through a straightforward mechanism: in a tighter marriage market, families with sons save aggressively to make their son a more attractive match. This pattern is strong enough in the data that the local sex ratio alone predicts regional savings rates, and the effect is estimated to account for as much as half of the rise in China’s household savings rate over the relevant period. As China's sex ratio has gradually become less skewed in recent years, this savings pressure has eased, a shift that lines up with the broader decline in China’s trade surplus since 2010.

Credit-starved firms save instead of borrow. China’s banking system has long favored state-owned enterprises, leaving many higher-productivity private firms with limited access to bank loans. Rather than scaling back investment, these firms compensate by financing growth out of their own retained earnings — effectively forcing them to save heavily to fund expansion that in a more market-driven financial system would be financed through borrowing. As these credit-constrained, butcproductive firms have grown to make up a larger share of the economy, this dynamic has pushed up the country’s overall corporate savings rate, further exacerbating China’s trade surplus. The recent growth of fintech lending — including loans to small and midsize firms from companies like Ant Financial — has eased some of this constraint, which the authors note lines up with the gradual decline in China’s surplus since the 2000s.

Fertility, aging, and a thin social safety net also boost saving. The one-child policy reduced the number of dependent children that families had to support, freeing up more income for savings. One estimate suggests holding family size at its 1970 level would have lowered China’s 2009 savings rate by seven percentage points. At the same time, rising life expectancy without a corresponding expansion of pension coverage has pushed households to save more for retirement on their own. That said, the authors urge caution: China’s social safety net as a share of GDP is roughly comparable to other countries at a similar level of development, like Mexico or Brazil. This suggests precautionary savings may be a contributing factor to China’s elevated savings rate (and by extension, its trade surplus) but is unlikely to be the dominant one.

Trade policy likely won’t address structural factors driving China’s surplus. If much of China’s trade surplus comes from a skewed marriage market and a credit-starved private sector rather than deliberate government policies, the researchers argue that the remedies favored by trading partners — higher tariffs, pressure to revalue the renminbi, and demands to cut subsidies — are unlikely to resolve China’s trade surplus. The more durable fixes, in their view, lie elsewhere: narrowing the sex ratio imbalance and improving the access to credit of private firms would address the root drivers of excess savings, though both would take years to show up in the data. In the meantime, they note, more aggressive stimulus aimed at lifting weak domestic demand offers the more realistic lever for narrowing the surplus in the near term — even if it leaves the deeper structural imbalance untouched.